")

")

")

Welcome, fellow seekers of financial peace! If the thought of managing your money feels overwhelming, you’re not alone. Many dream of having a clear roadmap for their finances, a way to feel in control rather than controlled by their earnings. The good news is that effective money planning doesn’t have to be complicated. This step-by-step guide will break down the essentials, empowering you to take charge and build a secure financial future.

Step 1: Understanding Your Current Financial Landscape for Effective Money Planning

Before you can chart a course, you need to know your starting point. This involves a clear understanding of your income and expenses.

- Track Your Income: List all sources of income, whether it’s your salary, freelance earnings, or investment returns.

- Monitor Your Expenses: This is crucial for effective . For a month, meticulously track every penny you spend. Use a notebook, a spreadsheet, or a budgeting app. Categorize your expenses (e.g., housing, food, transportation, entertainment).

- Analyze Your Spending Habits: Once you have a month’s worth of data, analyze where your money is going. Are there any surprises? Areas where you’re overspending? This insight is the foundation of successful money planning.

Step 2: Setting Clear Financial Goals with Your Money Planning

What do you want your money to do for you? Having specific, measurable, achievable, relevant, and time-bound (SMART) goals is vital for effective money planning.

- Short-Term Goals: These are goals you want to achieve within a year, such as saving for a down payment on a car, taking a vacation, or paying off small debts.

- Medium-Term Goals: These typically range from one to five years, like saving for a house, funding your child’s education, or starting a business.

- Long-Term Goals: These are goals that are five years or more away, such as retirement planning or building a significant investment portfolio.

Clearly defining your goals provides motivation and direction for your efforts.

Step 3: Creating a Budget: The Cornerstone of Money Planning

A budget is simply a plan for how you’ll allocate your money. It’s a powerful tool for achieving your financial goals through effective money planning.

- The 50/30/20 Rule: A popular budgeting method where 50% of your after-tax income goes to needs (housing, food, transportation), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment.

- Zero-Based Budgeting: Every rupee you earn is allocated to a specific category, ensuring your income minus your expenses equals zero.

- Envelope System: For variable expenses like groceries and entertainment, allocate a fixed amount of cash in envelopes. Once the envelope is empty, you can’t spend any more in that category. This can be a tangible way to stick to your money planning.

Choose a budgeting method that aligns with your lifestyle and helps you stay on track with your money planning.

Step 4: Prioritizing Savings and Investments in Your Money Planning

Saving and investing are crucial for long-term financial security and achieving your goals through diligent money planning.

- Emergency Fund: Aim to save 3-6 months’ worth of living expenses in a readily accessible account. This acts as a financial safety net for unexpected events.

- Automate Savings: Set up automatic transfers from your checking account to your savings or investment accounts each payday. This “pay yourself first” strategy makes money planning easier.

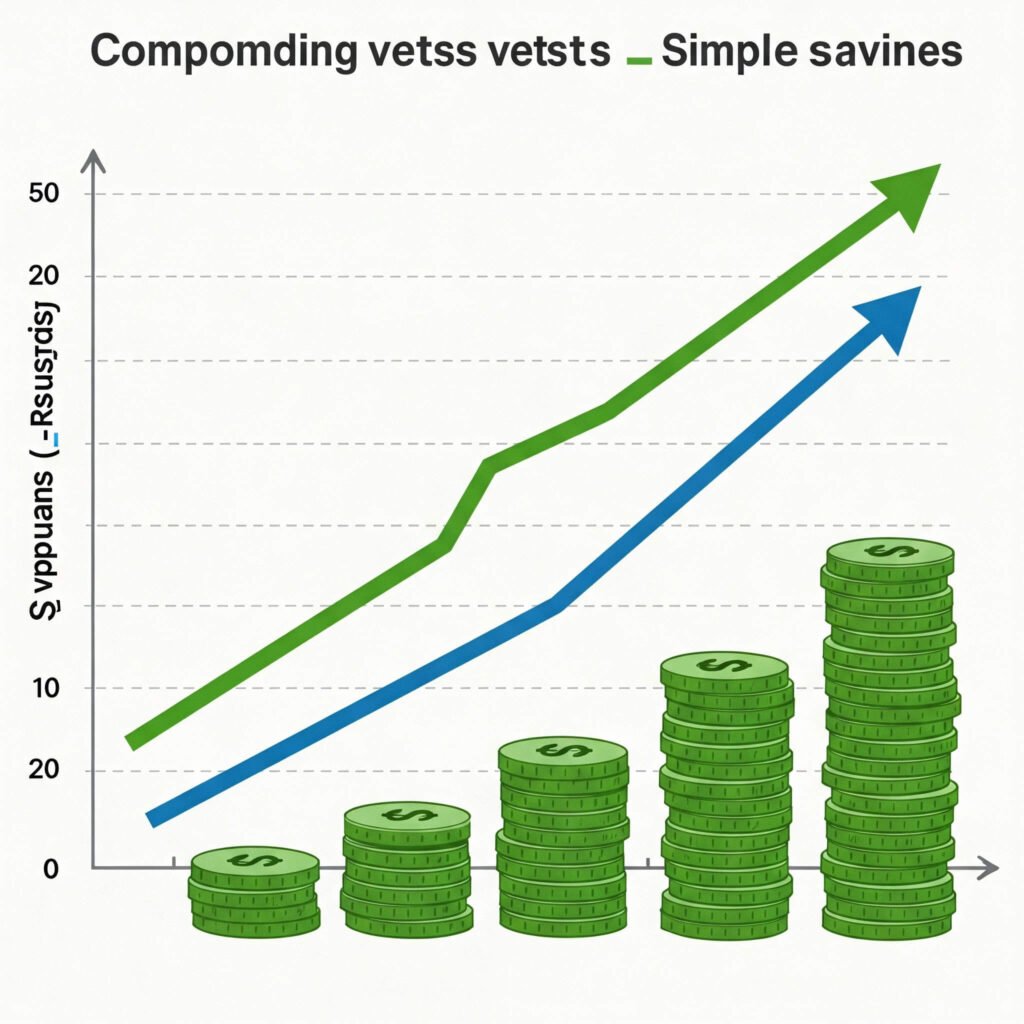

- Explore Investment Options: Depending on your risk tolerance and financial goals, consider various investment avenues like mutual funds, stocks, bonds, or real estate. Research thoroughly or consult a financial advisor. Understanding investment is a key aspect of advanced money planning.

Step 5: Managing Debt Effectively for Sound Money Planning

Debt can significantly hinder your financial progress. A solid strategy includes a plan to manage and reduce debt.

- List Your Debts: Make a list of all your debts, including the outstanding balance, interest rate, and minimum payment.

- Prioritize High-Interest Debt: Focus on paying off debts with the highest interest rates first to 1 save money on interest 2 charges. Use methods like the debt snowball or debt avalanche. 1. lyfeguard.com lyfeguard.com2. financebudget.exblog.jp financebudget.exblog.jp

- Avoid Taking on New Debt: As you work on paying down existing debt, be mindful of not accumulating more. This is a critical component of responsible money planning.

Step 6: Regularly Review and Adjust Your Money Planning

Money planning is not a one-time task; it’s an ongoing process. Your financial situation, goals, and life circumstances will change over time.

- Schedule Regular Reviews: Set aside time each month or quarter to review your budget, track your progress towards your goals, and make any necessary adjustments to your money planning.

- Adapt to Changes: Be prepared to adapt your plan when life throws curveballs, such as job loss, unexpected expenses, or changes in income. Flexibility is key to successful .

By following these simple steps, you can transform your relationship with money and gain greater financial control. Remember, money planning is a journey, not a destination. Start today, be consistent, and watch your financial well-being improve.

Outbound Reference Links:

- Link to a reputable financial education website, e.g., Investopedia

- Link to a government website offering financial literacy resources, e.g., the website of the Reserve Bank of India (RBI) or a similar financial regulatory body in your target region

- Link to a well-regarded budgeting app or software website, e.g., Mint or Personal Capital

")

{kind=link}