")

")

")

Like, I’m sitting here in my Denver rental (yeah still renting in my mid-30s, don’t @ me), sipping lukewarm coffee from yesterday’s Target mug, listening to the neighbor’s leaf blower at 8 a.m. on a Saturday, and thinking about how close I came to losing everything because I thought “eh, that’ll never happen to me.”

Spoiler: it almost did.

Two years ago I got hit with a car accident claim—other driver said I rear-ended them (I didn’t), lawyer got involved, medical bills ballooned, and suddenly my measly savings and 401(k) felt like they were on the chopping block. That was my wake-up call. Rich people don’t wait for the wake-up call. They build the damn fortress beforehand.

So here’s the real talk on asset protection strategies rich people use—and the ones I’ve actually started doing myself without needing to be a multimillionaire.

The fortress — solid, unshakeable, prepared long before any attack arrives.

Emergency Funds For High-Income Earners – Money Meets Medicine

Why Most People (Me Included) Ignore Asset Protection Until It’s Too Late

Seriously. We think lawsuits, creditors, divorce drama, or random medical malpractice claims only happen to other people.

I used to be that guy. “I don’t have enough to be worth suing.” Famous last words.

Turns out even $100k–$300k in home equity + retirement accounts + random savings is enough for someone to try. And lawyers love going after easy targets.

Rich folks? They treat asset protection strategies like brushing their teeth—non-negotiable daily habit.

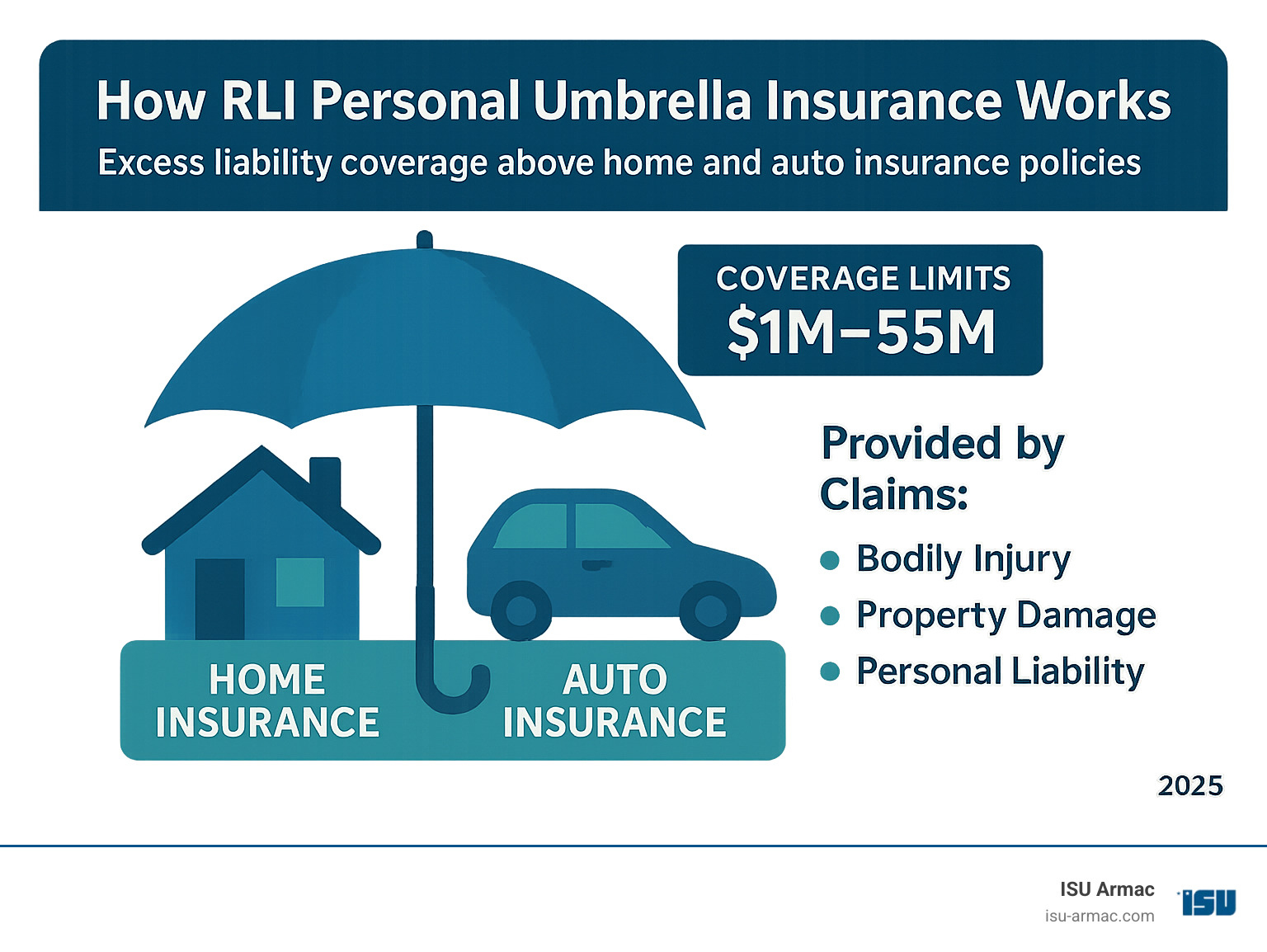

Umbrella Insurance: The Easiest Win I Actually Did First

This one’s boring but stupid-effective.

I added a $2 million umbrella policy through State Farm for like $350/year. Covers way beyond standard auto/home liability.

Last year when that accident happened, my lawyer basically said “you’re golden because of the umbrella.” The claim settled fast and low because the other side knew there was real coverage.

If you own a house, drive a car, have a dog, or even just exist in public, get umbrella insurance. It’s the cheapest asset protection strategy out there.

[Insert Inline Image 1: Slightly unusual angle—photo of a stack of legal documents on my actual kitchen table next to a cooling Domino’s pizza box, overhead smartphone shot, natural daylight, candid and imperfect.]

LLCs for Rental Properties or Side Hustles

I bought a tiny duplex in Aurora last year (FHA loan, barely scraped together the down payment).

Put it in an LLC immediately.

Colorado makes it pretty straightforward—file with the Secretary of State, get an EIN, operating agreement (ChatGPT helped me draft a basic one, then a lawyer tweaked for $400).

Now if a tenant slips on ice or whatever, they sue the LLC—not me personally. My personal bank accounts, car, 401(k) stay mostly untouchable.

Rich people layer LLCs like crazy—multiple properties in separate LLCs, businesses in their own entities. I’m not there yet, but one property in an LLC already feels like armor.

Homestead Exemption & Retirement Accounts

Colorado’s homestead exemption protects up to $250k (or $350k if over 60) of home equity from most creditors.

Not bulletproof (federal tax liens, mortgages, etc. still get you), but damn good for random lawsuits.

And retirement accounts? 401(k)s, IRAs, etc. have crazy-strong federal protection under ERISA and bankruptcy code.

I max my 401(k) partly because I like the tax break, partly because Uncle Sam basically says “good luck touching this.”

Rich people stuff as much as humanly possible into protected retirement vehicles.

Trusts (The Fancy Stuff I’m Not Rich Enough For… Yet)

Irrevocable trusts, domestic asset protection trusts (available in states like Nevada, South Dakota), offshore trusts—these are where the ultra-wealthy play.

They move assets out of personal ownership so even a judgment can’t reach them.

I talked to an estate attorney here in Denver about a domestic asset protection trust. He basically said: minimum $100k–$200k to make it worth it, plus ongoing fees, and you lose control of the assets.

12 Essential Questions to Ask Your Estate Planning Attorney

I’m not there yet. But I did set up a simple revocable living trust for my duplex and checking/savings—just so my family doesn’t have to deal with probate if I get hit by a bus tomorrow.

Baby steps.

The Messy Reality: Nothing Is 100% Bulletproof

Here’s the raw honesty part.

Asset protection strategies work best when done years before you need them. Courts can unwind transfers if they smell fraudulent conveyance.

I learned that the hard way reading case law after my accident scare—transfers made right before or during litigation get shredded.

Also, divorce? Most asset protection crumbles in divorce court. Ask me how I know (kidding… sort of… long story, ex from 2018 still haunts me).

And offshore stuff? Super expensive, IRS reporting nightmare (FBAR, FATCA), and if you’re not already ultra-high-net-worth, it’s probably overkill and risky.

Estate Planning for Women: 5 Essential Tips to Protect Your Legacy

What I’m Actually Doing Right Now (Flawed Human Edition)

- $2M umbrella policy — renewed last month.

- Duplex in single-member LLC.

- Maxing 401(k) + Roth IRA.

- Building cash in a high-yield savings (not protected, but liquid).

- Talking to a fee-only financial planner next month about whether a trust makes sense once I hit $300k net worth.

- Keeping really good records of everything because paper trail matters.

It’s not sexy. It’s not “Cayman Islands yacht money.” But it’s real, it’s legal, and it’s what regular-ish people can actually pull off.

Wrapping This Ramble Up

Look, asset protection strategies aren’t about being paranoid—they’re about sleeping better at night.

I used to wake up at 3 a.m. wondering if one bad day could wipe me out.

Now? Still anxious (because life), but way less.

If you’ve got a house, a car, kids, a business, whatever—start small. Umbrella policy today. LLC tomorrow. Retirement contributions always.