")

")

")

Asset allocation is honestly the only thing standing between me and complete financial chaos at this point in my life.

I’m sitting here in my kinda cramped apartment outside Raleigh, North Carolina – it’s February and the heat just kicked on again even though it’s 58 degrees outside because the thermostat is possessed – sipping lukewarm black coffee from a mug that says “World’s Okayest Investor” (gift from my sister, thanks Jess), staring at my brokerage app like it owes me money. And yeah, after about eight years of treating the market like a casino slot machine, I finally get why millionaires (the quiet ones, not the Lambo influencers) obsess over asset allocation more than anything else.

It’s boring. It’s not sexy. But damn if it doesn’t quietly compound while you’re busy panic-selling Tesla at -42% or FOMO-buying the next meme coin.

Why My Early “Asset Allocation” Was Basically Just Vibes

Back in like 2018 I thought asset allocation meant “put everything in whatever Reddit is screaming about this week.” My portfolio was 100% individual stocks – mostly tech, because duh growth – and a random sprinkle of crypto I bought after reading one too many r/wallstreetbets threads at 1 a.m.

Spoiler: it crashed. Hard. March 2020 wasn’t cute. I watched my “diversified” tech-heavy bag drop 35% in like three weeks while I stress-ate an entire family-size bag of Flamin’ Hot Cheetos on my couch in sweatpants that hadn’t been washed since February.

1,297 Desperately Stock Photos – Free & Royalty-Free Stock Photos from Dreamstime

That was the first time I actually googled “asset allocation” instead of just skimming Investopedia for five minutes and deciding I was basically Warren Buffett.

What Millionaires Actually Do (That I’m Slowly Copying)

From talking to people who are legitimately wealthy – not influencers, actual CPAs, engineers who retired at 45, my buddy’s dad who ran a small HVAC business in Ohio – the through-line isn’t fancy hedge funds or secret options plays.

It’s stupid-simple asset allocation dialed in over decades.

Here’s what I’m doing now that actually feels sustainable:

- Stocks (60-80% depending on how spicy I’m feeling that year) Mostly broad index funds. VTI or VOO for US total market/large cap. VXUS for a little international spice (usually 20-30% of the stock portion because yeah, home bias is real).

- Bonds (20-40%) BND or similar total bond market. I used to think bonds were for grandmas. Then 2022 happened and I was grateful for anything that didn’t drop 20%.

- Cash / “oh shit” fund 5-10% in high-yield savings or money market. Emergency fund separate, this is just dry powder for when everything inevitably gets weird again.

- The fun 5-10% Individual stocks, crypto, whatever dumb thing I want to play with. But capped. Hard. Because otherwise it becomes 60% and then we’re back to square one.

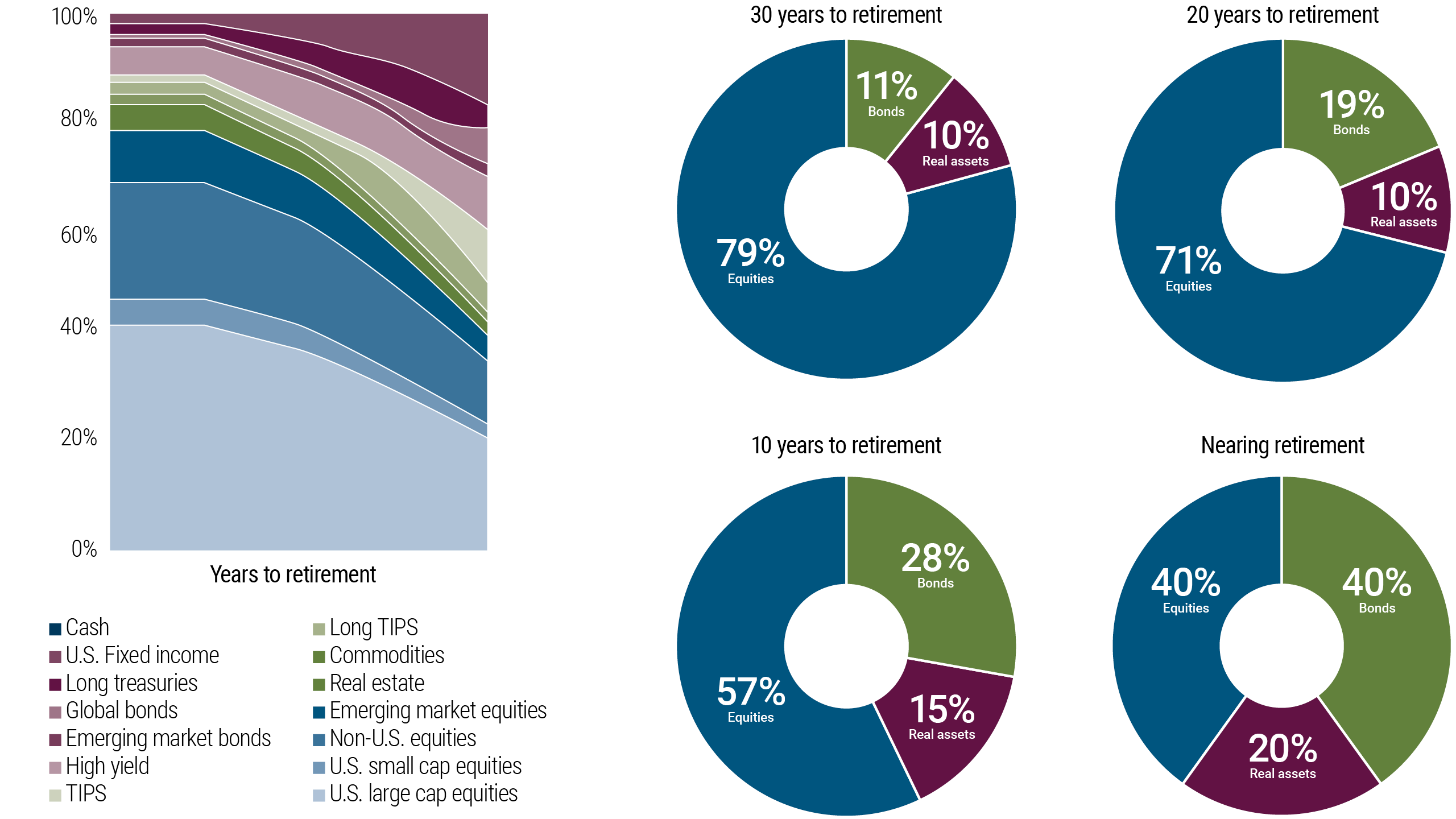

This shows conservative/moderate/aggressive pie charts with stocks/bonds/cash breakdowns—your “spicy” years lean toward the aggressive side (high stocks), calmer years closer to moderate.

Uncovering the Benefits of Asset Allocation | PIMCO

For more on why simple beats clever long-term, check out this Vanguard study on portfolio diversification – it’s dry but it slaps you with data.

Finance Diversification Stock Illustrations – 8,045 Finance Diversification Stock Illustrations, Vectors & Clipart – Dreamstime

Rebalancing: The Part I Still Kinda Hate

Every year (or when something drifts more than 5-10%) I force myself to sell winners and buy losers.

Last December I had to sell a chunk of my tech ETF that had run up stupidly and move it into bonds. Felt like punching myself in the wallet. But then bonds rallied a bit in early 2025 and I didn’t hate life as much.

It’s mechanical. It’s unsexy. It’s exactly why it works.

My Current Messy-but-Getting-Better Allocation (as of right now)

- 68% US & Int’l Stocks (mostly VTI/VXUS)

- 24% Bonds (BND)

- 8% “Play money” – split between a couple individual names and Bitcoin ETF because I’m weak

Not perfect. Not even close to what the Bogleheads forum would approve. But it’s mine, it’s consistent, and it’s boring enough that I actually stick with it.

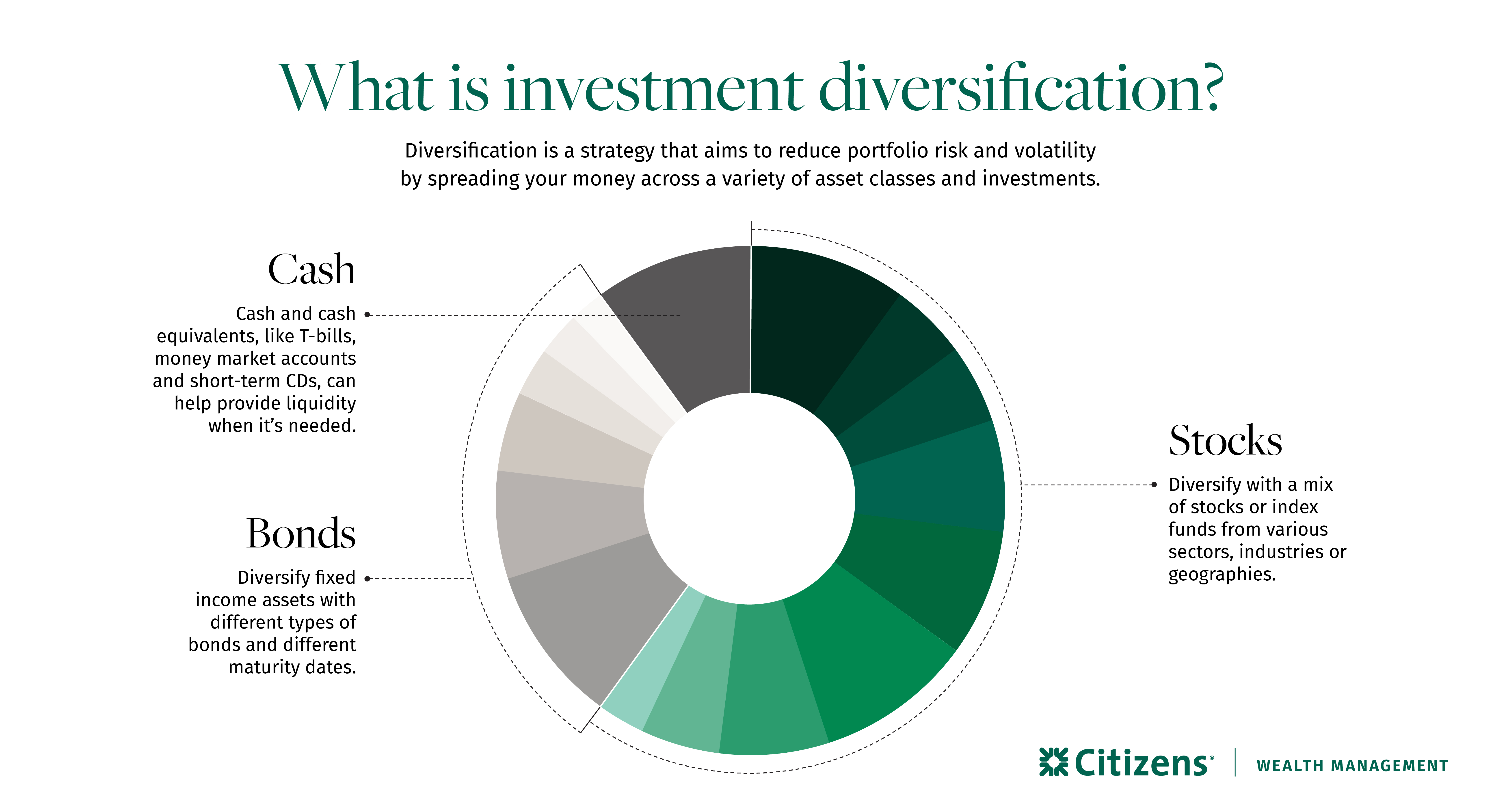

Investment Diversification: How it Works and Why it’s Important | Citizens

The Millionaire Mindset Shift I Had to Force

The real unlock wasn’t the percentages.

It was accepting that asset allocation isn’t about getting rich quick – it’s about not getting poor quick.

Millionaires (the ones I know personally) treat their portfolio like a slow-cooker meal: set it, check occasionally, don’t keep opening the lid to see if it’s done yet.

I still fight the urge to tinker. Yesterday I almost dumped more into small-cap value because some podcast said it’s “undervalued.” Then I remembered 2022 and closed the app.

Wrapping This Ramble Up

Look, I’m not a millionaire. Not even close. But I’m not broke anymore either, and for the first time my net worth chart trends up instead of looking like a dying EKG.

If you’re still treating investing like a video game, try this: pick a simple asset allocation that matches how much market vomit you can actually stomach, automate contributions, rebalance once a year, and then go touch grass.

It won’t feel exciting. But neither does paying your electric bill on time, and that still feels better than the alternative.

What’s your current asset allocation looking like? Drop it in the comments (or just tell me I’m an idiot, that’s fine too). Seriously curious.

")